The first number an insurer puts in front of you is almost never what your case is worth. It's what they can settle the case for today, before you've seen a specialist, before your wage loss is fully documented, and before a lawyer has had time to argue with them about fault. The gap between that first number and a fair one is often substantial — routinely 2× or 3×, sometimes more — and closing that gap is most of what a personal-injury attorney is paid to do.

What follows is how that number is built, on both sides. It is not legal advice for your specific case; it is the framework that attorneys and adjusters use to negotiate, so you can read the offer you've been given and know roughly where it sits.

A car-accident settlement is economic damages plus non-economic damages, adjusted for your share of fault and capped by the at-fault driver's policy limits. Everything else is commentary.

Economic damages: what you can put on a receipt

Economic damages are the part of your case a calculator can settle. They include your medical bills (past and reasonably foreseeable future), your lost wages, your lost earning capacity if your injury changes what work you can do, and incidental out-of-pocket costs — mileage to physical therapy, prescriptions, assistive equipment. Insurers rarely fight hard on the existence of these; they fight on the size.

The three line items adjusters usually compress

- Future medical care.If your doctor says you'll need three more years of PT, the insurer will often value one. Get the prognosis in writing.

- Lost earning capacity. A back injury that keeps a roofer off roofs is a different number than a back injury for a remote worker. Adjusters assume the smaller case.

- Household services.The cost of things you can't do yourself while healing — yard work, childcare, cleaning — is recoverable in most states and routinely forgotten.

The economic number is where most settlements are won or lost before anyone even argues about pain.— Common refrain among plaintiff attorneys

Non-economic damages: the part that hurts

Non-economic damages cover the parts of an injury that don't produce receipts — pain, suffering, emotional distress, loss of enjoyment of life, and, in a permanent injury, loss of consortium for your partner. They are real, they are compensable, and they are genuinely difficult to value.

In practice, most adjusters and attorneys calculate them two ways: a multiplier of economic damages, or a per-diem based on the days you were in meaningful pain. The multiplier method is the more common of the two.

The multiplier, explained

The multiplier is a number between roughly 1.5 and 5, applied to your economic damages. Minor soft-tissue cases sit near the bottom. Cases with surgery, ongoing treatment, and documented long-term impact sit near the top. A catastrophic injury — permanent disability, disfigurement, traumatic brain injury — can push past 5, though at that point you are no longer in routine-settlement territory.

So: $18,000 of economic damages at a 3× multiplier is a case worth about $72,000 before any fault reduction or insurance cap. The adjuster's spreadsheet will argue 1.5× and $12,000 of economic damages; your attorney will argue 3.5× and $22,000. Most settlements land somewhere between those two positions.

Want a real person to look at the offer you have?

A four-minute free review gets your case in front of our intake team. If the number you've been offered is low, we'll say so. If it's fair, we'll say that too.

Start free intake reviewSeven factors that actually move the number

- Severity of injury. Documented, imaged, specialist-verified. What the record says, not what you told the adjuster on day one.

- Length of treatment. A three-week chiropractor course is a different case than a nine-month orthopedist course. Consistency matters.

- Liability clarity. Was the other driver clearly at fault? Rear-ended at a light is a different case than a disputed left turn.

- Wage loss documentation.Pay stubs, employer letters, W-2s. If you're self-employed, tax returns and invoices for the two years prior.

- Venue. Juries in different counties return very different numbers for identical facts. Adjusters know your venue before you do.

- The defendant. A large commercial defendant (a trucking company, a rideshare platform) has deeper coverage and more reputational incentive to settle than an individual driver at state minimums.

- Your patience. Insurers settle faster cases for less. Cases that credibly might go to trial settle for more.

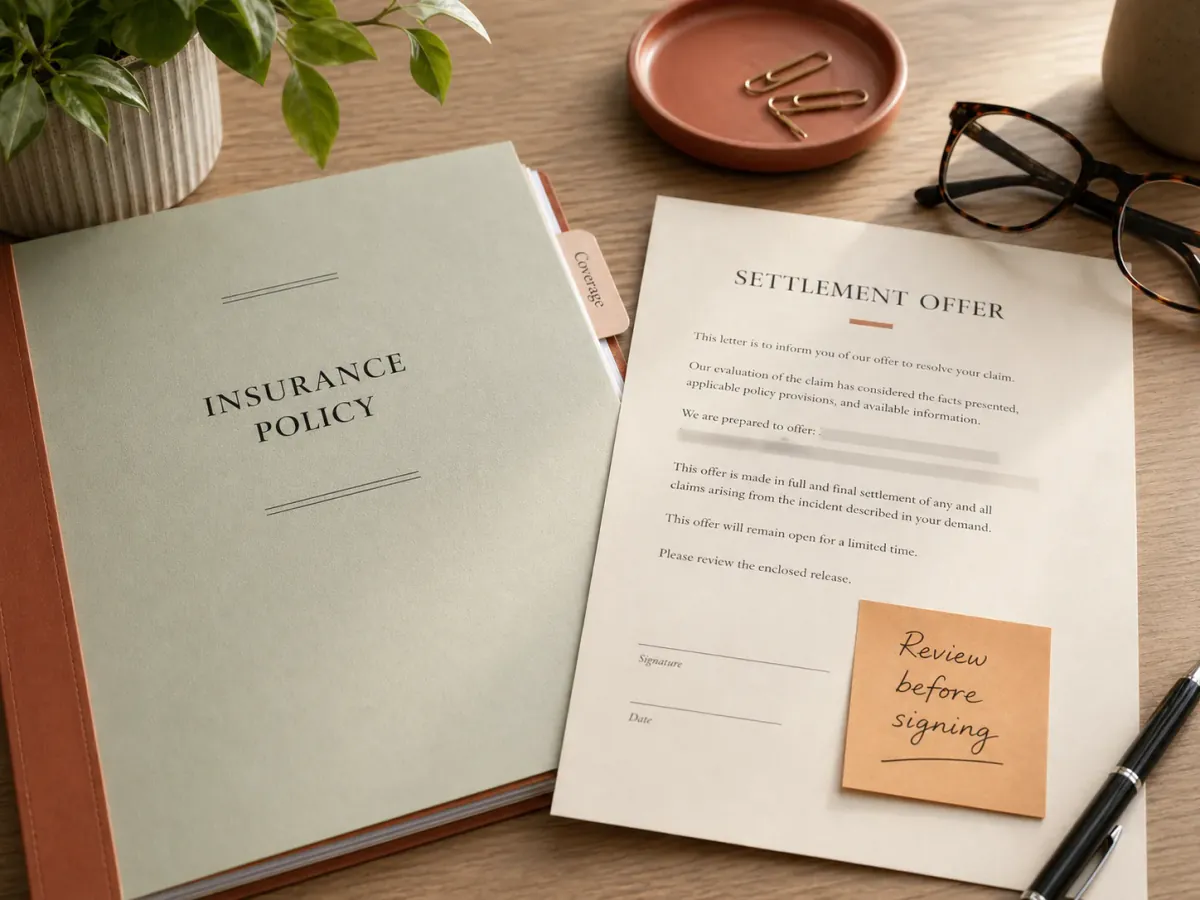

Policy limits: the hard ceiling

Every settlement has a ceiling, and that ceiling is usually the at-fault driver's liability insurance limit. State-minimum policies are shockingly small — in Nevada, $25,000 per person is legal. If your damages exceed the limit, you have three options: accept the policy limit and release the claim, pursue the driver personally (which in most cases recovers nothing), or file a claim against your own underinsured-motorist coverage if you carry it.

Economic damages plus the value of pain and disruption.

The number drops if the insurer can assign part of the fault to you.

The at-fault driver's policy often sets the practical ceiling.

What to do today

A short, specific checklist.

- Get a copy of your medical records. Request them from every provider — ER, primary care, specialists, imaging. You are legally entitled to them.

- Document lost wages. Ask HR for a letter stating the days you missed and your rate. Save pay stubs from the month before and the month of the accident.

- Start a symptom journal.Ten seconds a day. "Back pain 6/10, couldn't lift toddler, missed yoga." Cheap, powerful evidence of non-economic damages.

- Do not give a recorded statementto the other driver's insurer without counsel. You are not legally required to.

- Get a case review. Not every case needs a lawyer — but you should find out which category yours is in before signing anything.

The worst time to make a decision about your settlement is in the first week, when your phone is ringing and the adjuster sounds friendly. The best time is once your medical picture is clear and your wage loss is documented. That gap — usually 30 to 90 days — is where you protect the value of your claim.